Flying Tulip April Update

The end of April marks two months since Flying Tulip launched. Since then, the protocol has moved from launch into active rollout, introducing its on-chain PUT execution and AUM system, launching ftUSD as its stablecoin and settlement layer, deploying Margin Lending on Sonic, and enabling the first delta-neutral strategies.

As our March Update explained, Flying Tulip introduced Perpetual PUTs, validating a novel DeFi capital-raising and operating model which protects initial investors through a redemption mechanism, granting holders the right to exit their position and redeem their original capital in the same token and amount. The capital backing the PUTs has since been deployed into conservative, unwind-friendly strategies, with the resulting yield helping fund the continued development of the ecosystem, infrastructure, and operations.

Flying Tulip is deploying a sequence of integrated, novel financial products that reuse the same pricing, collateral, and settlement infrastructure. Next planned releases include expanding Margin Lending and deploying delta-neutral strategies on Ethereum; launching Flying Tulip Spot, an adaptive trading engine that routes orders between a dynamic AMM and an on-chain order book (CLOB) to achieve the best execution and liquidity; rolling out Leverage Trading; and Total Return Swaps (TRS).

TRS are intended to offer perp-like leveraged exposure with ftUSD as settlement collateral, but through a more controlled, spot-linked design that reduces reliance on a traditional perp engine and avoids auto-deleveraging (ADL).

ftUSD minted: $1.49M total

— $761K on Ethereum

— $727K on Sonic

ftUSD APY:

— 6.16% on Ethereum

— 4.18% on Sonic

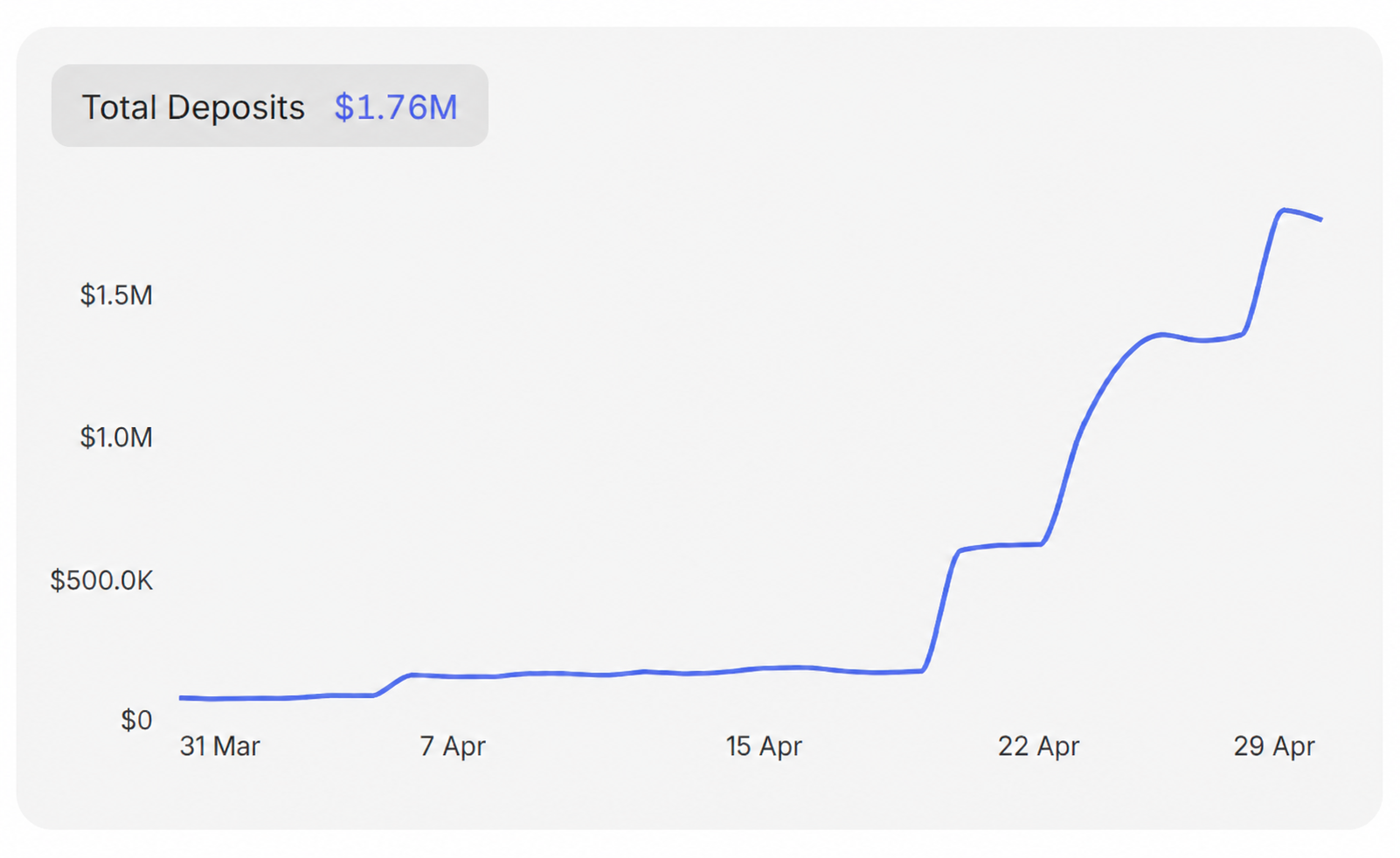

Lend Supply: $1.76M

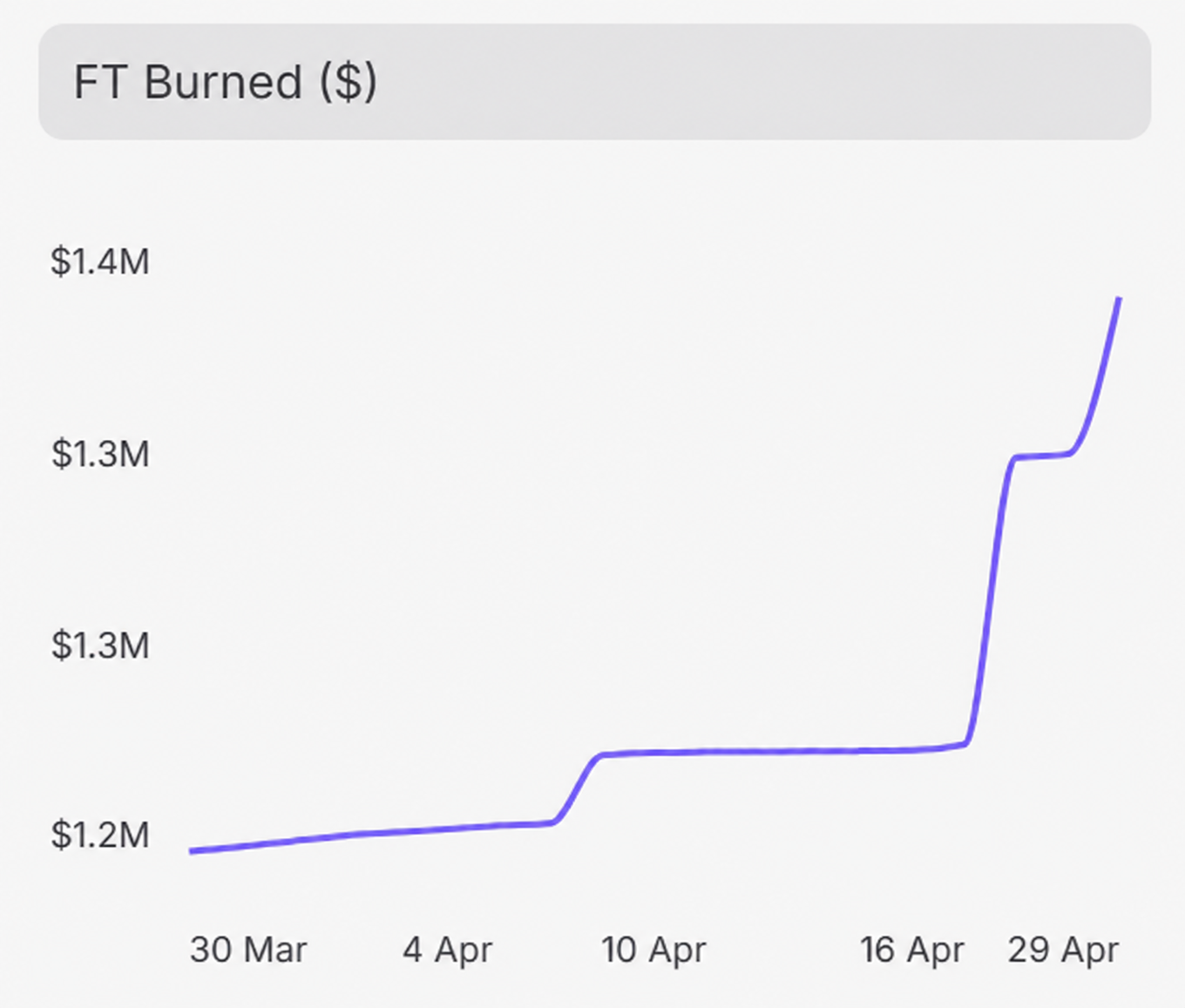

FT bought back and burned: 12,185,612.71M ($1.4m)

All-time yield generated: $750k

Total backing capital: $64.02M

For the latest figures, see the ftUSD Dashboard and Allocation Dashboard.

Margin Lending

In April, we launched Margin Lending, a key building block for Flying Tulip, and an important step toward scaling ftUSD. Margin Lending makes possible delta-neutral strategies for ftUSD, while establishing the margin infrastructure needed for spot and leveraged trading.

In general, yield on Margin Lending comes from two sources. First, the portion of supplied assets that is borrowed earns borrow interest paid by borrowers. Second, the portion that is not borrowed is deployed into yield strategies, so idle liquidity continues generating return. As a result, deposit APY reflects both borrow-side income and strategy yield on unused capital, rather than borrow demand alone.

Monitor Lend Stats: https://flyingtulip.com/lend/dashboard

DefiLlama Dashboard: https://defillama.com/protocol/flying-tulip-lend

Suppliers deposit assets and begin accruing interest, while borrowers post collateral and take loans within loan-to-value limits. Under the hood of Margin Lending, these limits and rates are market-aware rather than hard-coded. When the market is calm and deep, your borrowing power is more generous. As volatility rises or depth thins, your available LTV gracefully tightens.

Maintenance-based lending represents a major DeFi evolution beyond LTV-based lending. By making risk parameters responsive to market conditions, it enables a broader set of hedged strategies that can move from active management toward more passive management, reducing stress for borrowers while improving yield opportunities for depositors.

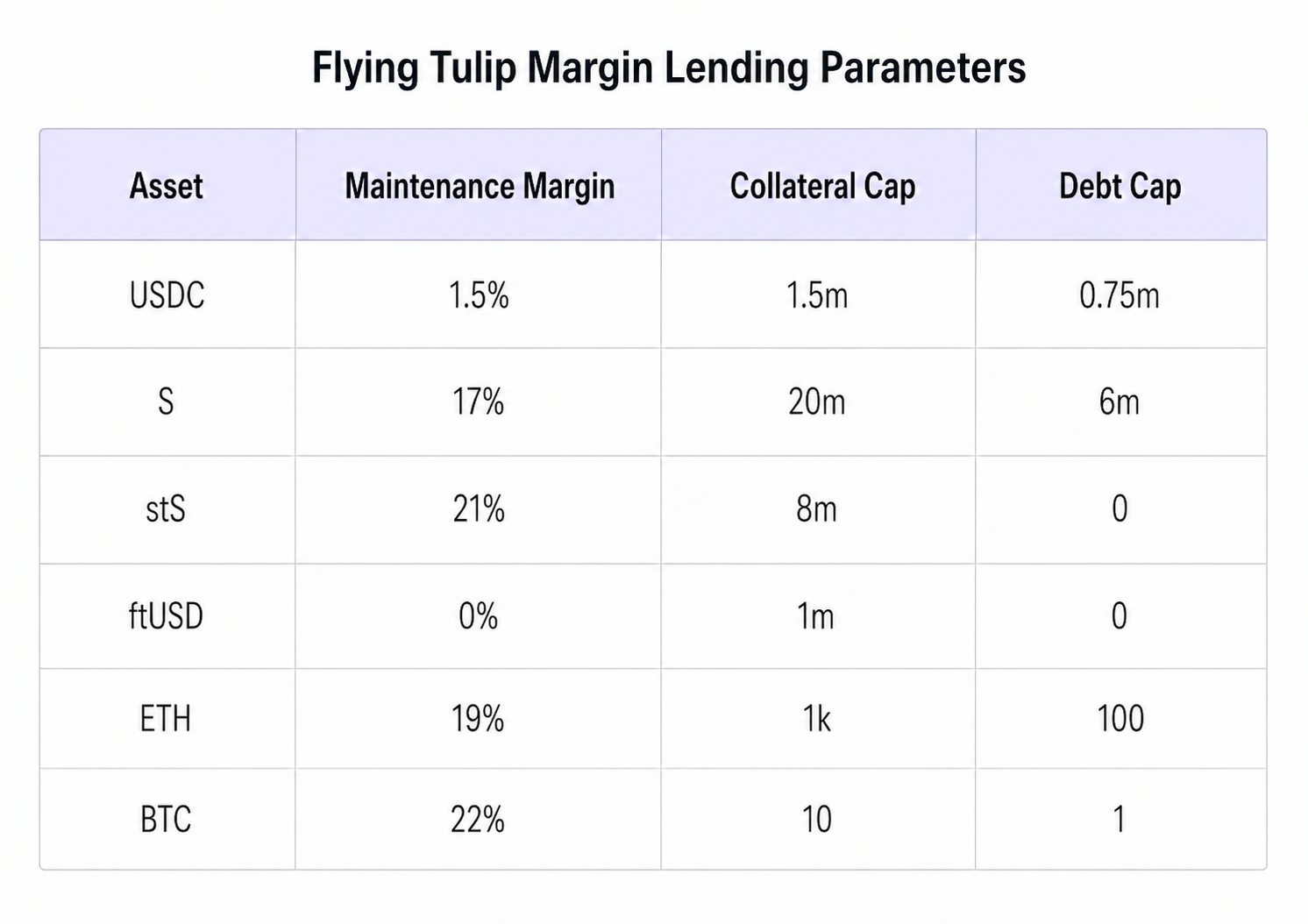

For each asset in Margin Lending, three parameters are considered:

- Maintenance Margin: the minimum safety buffer a position must keep when that asset is used in the system. If account health falls too low relative to that requirement, the position can be liquidated.

- Collateral Cap: the maximum total amount of that asset the protocol currently allows to be supplied as collateral.

- Debt Cap: the maximum total amount of that asset the protocol currently allows to be borrowed.

Like the rest of the Flying Tulip stack, Margin Lending routes all generated cashflows through the protocol's token‑first model. Lenders receive their share as FT‑denominated distributions, obtained through secondary market buybacks.

Margin Lending initially launched in a guarded, capped rollout on Sonic, with no active incentives. In May, the focus will be on moving active products toward full production scale to grow ftUSD supply and further increase Margin Lending TVL.

ftUSD limits increased.

— flyingtulip.com (@flyingtulip_) April 27, 2026

Ethereum & Sonic caps increased from 1,000,000 to 5,000,000.

Earn 8.38% on USDT & USDC depositing into ftUSD;

Earn: https://t.co/V3rNljYt03

Stats: https://t.co/ogvxnlVhBK pic.twitter.com/OM4ENJxlkN

Delta-Neutral Strategies

As Margin Lending is maturing as a product, ftUSD is expanding beyond passive wrapper yield into delta-neutral strategies that pair staking derivatives with their underlying assets, such as stETH/ETH, stBNB/BNB, stAVAX/AVAX, and stS/S. These strategies are designed to capture staking yield while minimizing directional exposure. Delta-neutral strategies are currently deployed on Sonic, with plans to bring them to Ethereum as Margin Lending scales further.

So many new building blocks required to get here onchain. You can do this strategy with active management (in a limited fashion onchain), but no passive options, so we had to first rebuild an issuance / settlement layer (ftUSD), that can then feed into a margin based lending… https://t.co/BEBzozAh52

— Andre Cronje (@AndreCronjeTech) April 15, 2026

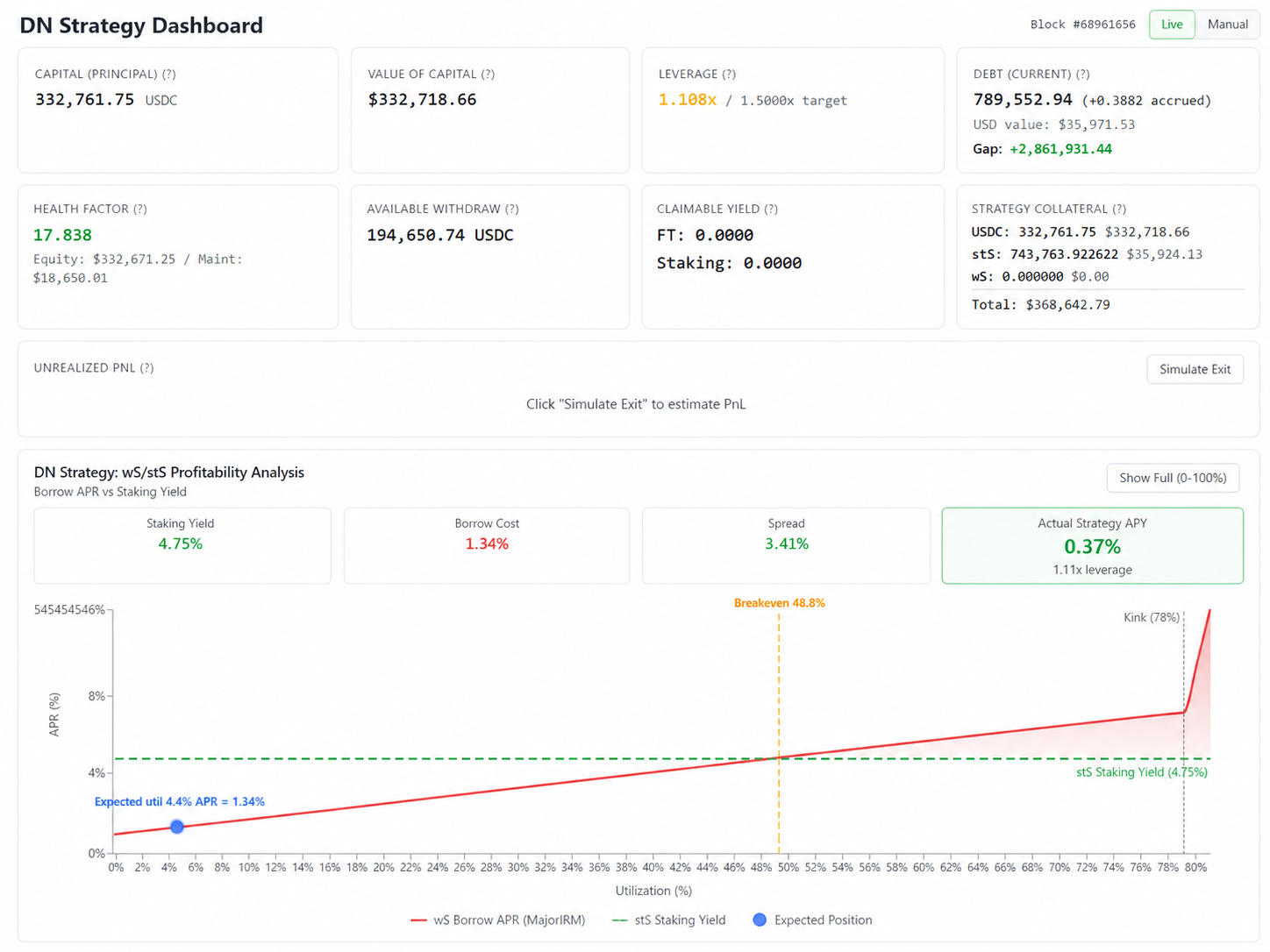

On Sonic, the strategy deposits USDC as collateral into the Flying Tulip Positions Manager, or PM, earns FT rewards on the supplied collateral, borrows wS, the native Sonic token, against that collateral, and stakes the borrowed wS into stS. This generates staking yield while hedging wS price exposure through the borrowed position. Target leverage is configurable, for example at 1.50x.

All FT yield (from both lending interest and PM rewards) flows directly to sftUSD stakers. No FT accumulates idle in the strategy or treasury.

FT Token

FT is the native token of Flying Tulip and is integrated across the entire product suite, with the token model designed to convert all value generated by the platform into direct demand for FT.

As a reminder, primary sale participants and holders of Perpetual PUT Options purchased on the Flying Tulip's PUT Marketplace, maintain the redemption option: They can exit any portion of the PUT with the same asset and amount originally contributed. There is no deadline to exercise this option.

Holders of Perpetual PUT Options maintain the option to exit their position. For example, if they deposited $1000, they can redeem $1000. If they deposited 3.5 ETH, they can redeem 3.5 ETH.

Perpetual PUT Options contain both the redemption option and the FT Token. A holder can also choose to withdraw the FT from the PUT, but doing so invalidates the redemption option. This generally only makes economic sense if the market value of the FT exceeds the value of the underlying redeemable capital (or the price that could be achieved on the PUT Marketplace).

FT purchased on secondary markets is volatile and does NOT carry a redemption option. When a PUT is invalidated, the backing capital is released and used by the protocol to buy FT on the open market at the average redemption value, or NAV, of withdrawn PUTs. The purchased FT is then burned. As a result, secondary-market FT has structural support through buybacks, but not a guaranteed price floor.

As of April 30, 12,185M FT has been bought from the market and burned.

The primary sale price of FT was $0.10, with stablecoins and ETH accepted as collateral. Because ETH is currently trading below its sale-period price, the average value of capital released from invalidated ETH-backed PUTs is below $0.10 per FT, and so is the system buyback price.

There is currently about $1.3 million in capital from withdrawn FT designated for buybacks and burns. Once Flying Tulip Spot goes live, that capital is intended to be deployed as ftUSD-denominated limit orders, at NAV. The underlying collateral remains in yield-generating strategies, with the resulting yield accruing to sftUSD stakers.

In addition, revenue and fees generated across Flying Tulip products, and eventually PUT yield, are also converted into demand for FT through open-market buybacks, at spot price. A large share of these purchases is burned, reducing supply while reinforcing demand for the token.

As Flying Tulip products become fully deployed and integrated, secondary-market FT pricing should increasingly reflect the protocol’s underlying cashflows, buyback demand, and supply reduction mechanisms.

Finally, once protocol revenue is sufficient to sustain team operations and reaches $3,500 per day, Flying Tulip plans to burn all unallocated and divested supply. This currently represents more than 93% of total supply, or 9,333,329,982 FT.

Security as a Top Priority: Introducing Circuit Breakers

On April 18, 2026, Kelp DAO suffered a major security breach that resulted in the loss of approximately 116,500 rsETH. A forged LayerZero message on a 1-of-1 Decentralized Verifier Network, or DVN, route caused rsETH to be released from Kelp’s Ethereum-side adapter without a corresponding burn on the source chain. The attacker then used the rsETH on Aave to borrow ETH.

The Flying Tulip team responded immediately. To protect PUT holders, the team withdrew ETH from Aave as soon as liquidity dropped below the minimum threshold. As an additional precaution, the team paused FT LayerZero bridges until the root cause of the rsETH incident could be identified.

As a result, Flying Tulip has no exposure to the incident, and there is no impact on FT or Perpetual PUT holders.

Aave’s system relies on technical due diligence and DAO asset approvals, but it was not designed to prevent this type of incident at the protocol level. This is why Flying Tulip introduces circuit breakers: proactive rate-limiting mechanisms designed to prevent a threat actor from rapidly draining user funds and to give the team time to respond during an incident.

Circuit breakers continuously monitor flows of funds leaving the protocol and are implemented for PUT withdrawals, ftUSD redemptions, and Margin Lending withdrawals. If outflows for a given asset spike beyond the normal range over a short period, a pattern often associated with security attacks, the circuit breakers automatically limit the rate of subsequent withdrawals.

— Dunking Squirrel (@DunkingSquirrel) April 21, 2026

Community-made tweet on Flying Tulip's circuit-breaker mechanism.

At Flying Tulip, the security of user funds is the top priority. Products are launched conservatively, beginning with guarded and capped phases that validate mechanics under real market conditions before capacity and complexity are expanded.

In addition to implementing a circuit breaker and launching capped, ftUSD also includes a competitive 0.1% mint and redeem fee. Beyond generating protocol revenue, this fee is primarily designed as a security mechanism. By making the fee exceed the gas cost of a potential attack, the protocol can prevent cross-asset drainage, wash-trading DDoS attacks, and cross-asset arbitrage at the expense of the protocol.

Before launching, Flying Tulip opened the code to competitive review from hundreds of independent security researchers at Sherlock bug bounty and audit platform, with $100,000 USDC in rewards on the line. The contest wrapped up with zero valid Medium or High severity findings, making it one of the cleanest contest outcomes seen on Sherlock.

Before launch, @flyingtulip_ brought its ftPUT contracts to Sherlock for a final external review.

— SHERLOCK (@sherlockdefi) April 30, 2026

The goal was simple: put high-value code in front of a massive researcher community before real capital moved through it.

Full writeup below. https://t.co/wQ52RprgLh

Flying Tulip also maintains a live bug bounty on Sherlock with rewards of up to 1,000,000 USDC, open to all researchers directly incentivizing them to identify and disclose vulnerabilities which could lead to loss of user funds.

Investor Update

Flying Tulip introduced a token-first financial architecture in which tokens enter circulation only when a Perpetual PUT Option is backed by capital. There are no bonus tokens distributed to early investors and no free tokens allocated to the team. This structure allows PUT holders to exit their position and redeem the backing capital at any time, without creating a sell pressure, or negatively impacting those who remain.

In fact, every exit (and withdrawal) strengthens the position of those who remain, since a larger share of the un-allocated supply will ultimately be burned.

Since the end of the sale and the launch of Flying Tulip, more than $140 million has been redeemed by primary sale participants. VCs that exercised the PUT Option have primarily cited liquidity constraints, while larger outflows also followed the Drift Protocol exploit on April 1, the Mythos announcement on

April 9, and the rsETH exploit on April 19.

Although Flying Tulip implements multiple safety mechanisms designed to prevent large-scale withdrawals and limit the impact of major exploits, the reaction and perspective of participating funds is understandable. Their priority is to protect the capital of their own investors, especially in an unstable market.

From Flying Tulip’s perspective, these PUT outflows are expected. The amount raised initially exceeded the protocol’s immediate funding needs by design, providing flexibility for staged deployment, liquidity management, and future protocol growth rather than merely covering the minimum required capital.

We are grateful for the capital initially locked by both remaining and exiting investors, and the yield generated has been put to productive use. In less than two months since launch, Flying Tulip has launched the ftUSD stablecoin, rolled out Margin Lending, and deployed delta-neutral strategies, with metrics rising across the board.

At the time of writing, the total backing value of tokens locked in PUT Options is $64 million, and all-time yield generated is $750k. April spending was further reduced, meaning operating income remains above cash burn. At current yield levels, Flying Tulip would only need to begin considering alternative funding options at PUT TVL of about $30m-40m.

PUT yield, however, was always intended only to bootstrap the project. Over the longer run, product revenue is expected to fund team operations and ecosystem development. In May, Flying Tulip continues its mission to launch novel on-chain products, and scale existing products, which are already starting to generate revenue and fees.

Links

Socials

- Website: https://flyingtulip.com

- X/Twitter: https://x.com/flyingtulip_

- Discord: https://discord.gg/flyingtulip

Products

- PUT Marketplace: https://marketplace.flyingtulip.com

- ftPUT: https://flyingtulip.com/allocation/dashboard

- ftUSD: https://flyingtulip.com/ftusd/dashboard

- Margin Lending: https://flyingtulip.com/lend/dashboard

Documentation

- FT Docs: https://docs.flyingtulip.com/product-suite/ft-token

- ftUSD Docs: https://docs.flyingtulip.com/product-suite/ft-usd

- Roadmap: https://docs.flyingtulip.com/roadmap

- Contract addresses: https://docs.flyingtulip.com/contract-addresses

Community Resources

- Supply Dashboard (Tracks FT buybacks, burned, circulating, and non-circulating supply): https://ftdashboard.xyz

- Advanced PUTs Marketplace Dashboard: https://ftdashboard.xyz/puts-marketplace.html

- Circuit Breaker Status + Telegram Alerts: https://ftcircuitbreaker.com